The State of the Network

Hyperliquid’s app ecosystem has crossed a defining threshold. Every new builder or operator doesn’t dilute the network, it compounds it. Hyperliquid has reached CEX-class execution reliability, but without custody risk. Liquidity is not pooled across bridges or sidechains; it’s native and synchronous within one global state.

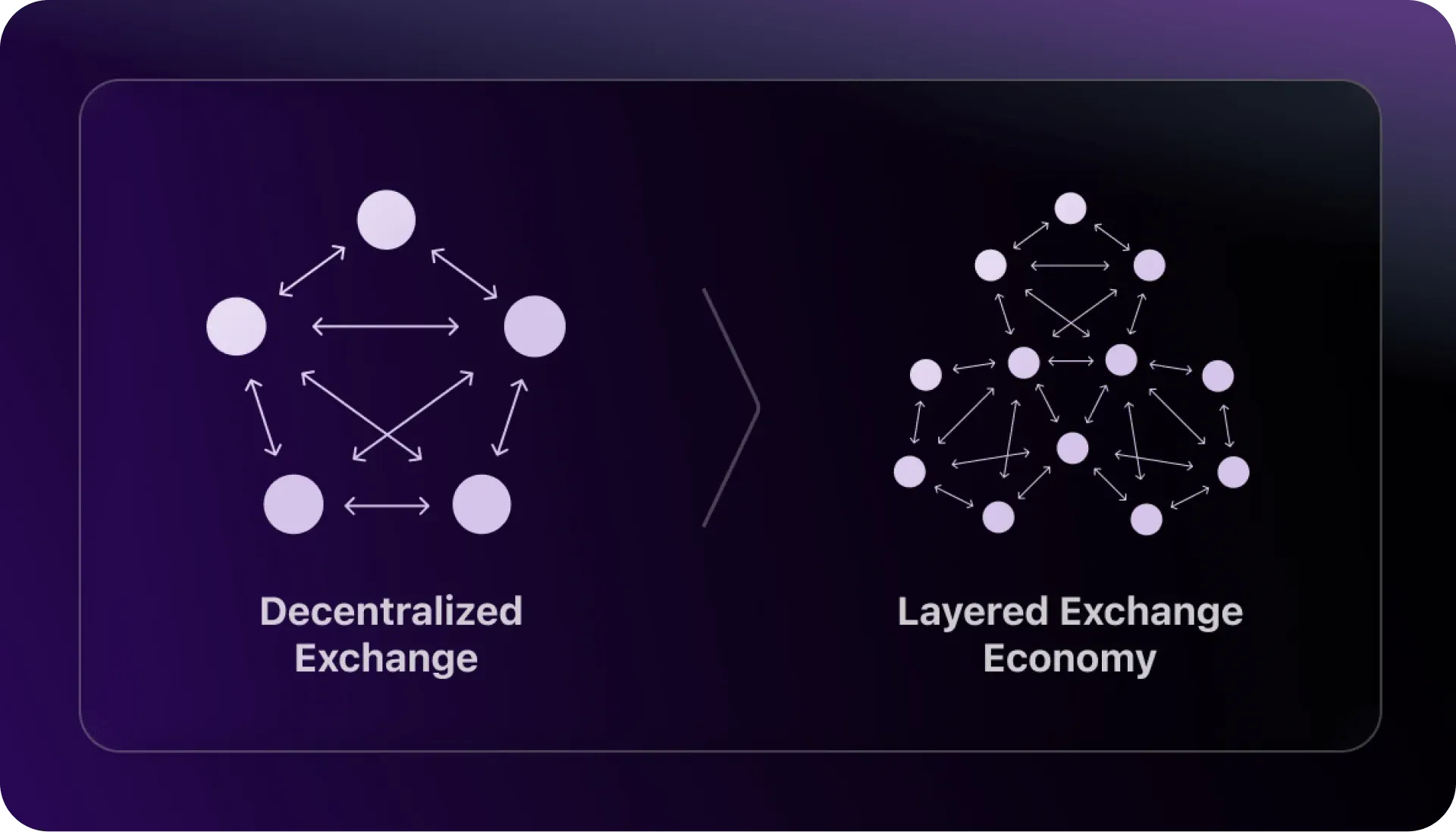

Hyperliquid is no longer one exchange. It’s a network of micro-exchanges, each competing on UX, routing algorithms, and community reach, all under a shared liquidity layer. Daily payouts now behave like recurring platform revenue, not sporadic bursts of retail speculation.

But the real story is architectural: liquidity, compute, and distribution are no longer separate businesses, they are one vertically integrated, programmable stack. Builders acquire users, validators secure performance, operators provision markets, and all earn directly from the same transaction loop.

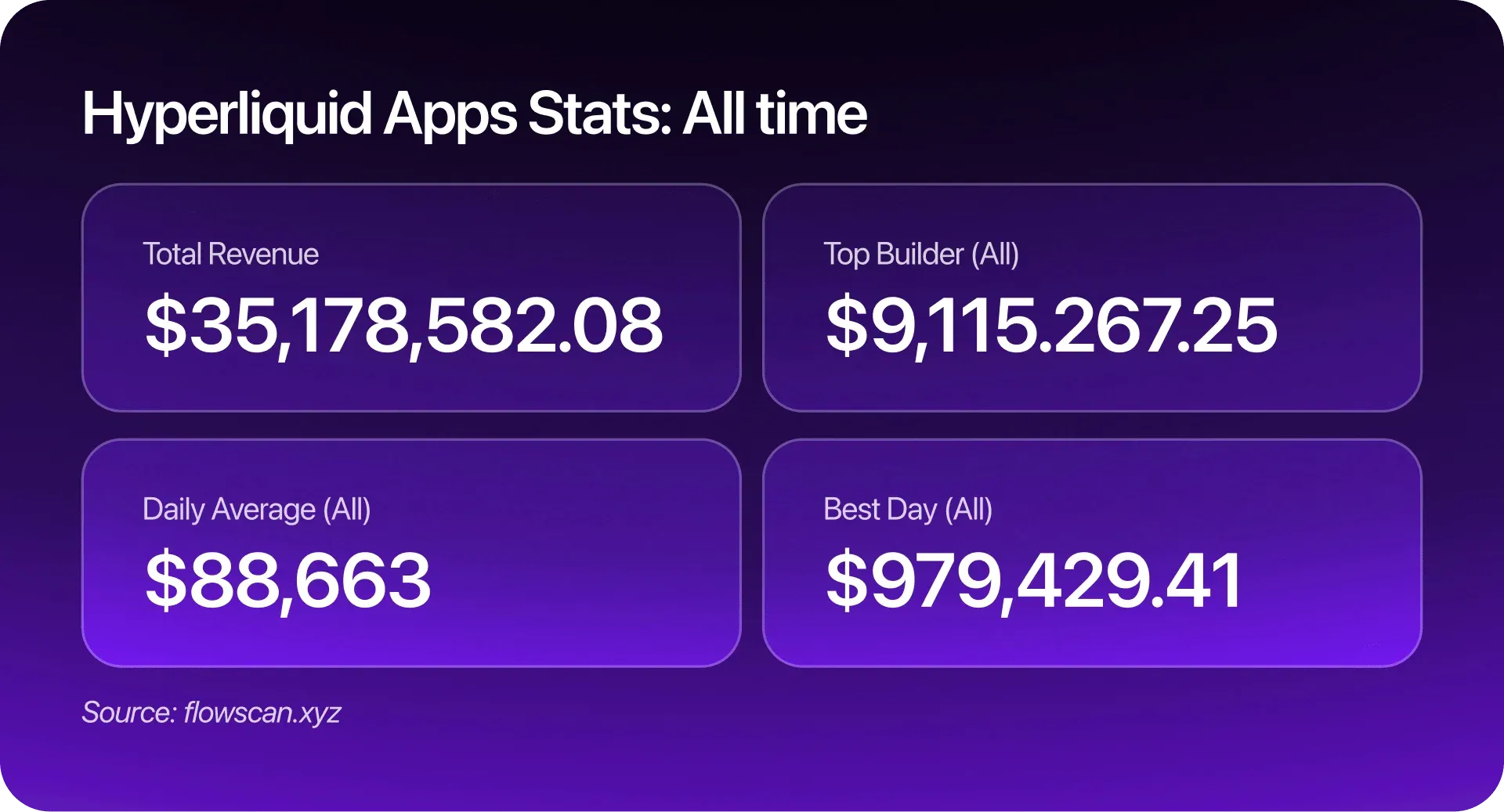

We have reached a point where Hyperliquid’s app ecosystem has become self-sustaining. With $35 million paid out, 231K users, $317 billion monthly volume, and hundreds of millions in collateral, the protocol now rivals mid-tier centralized exchanges on every operational metric except marketing spend.

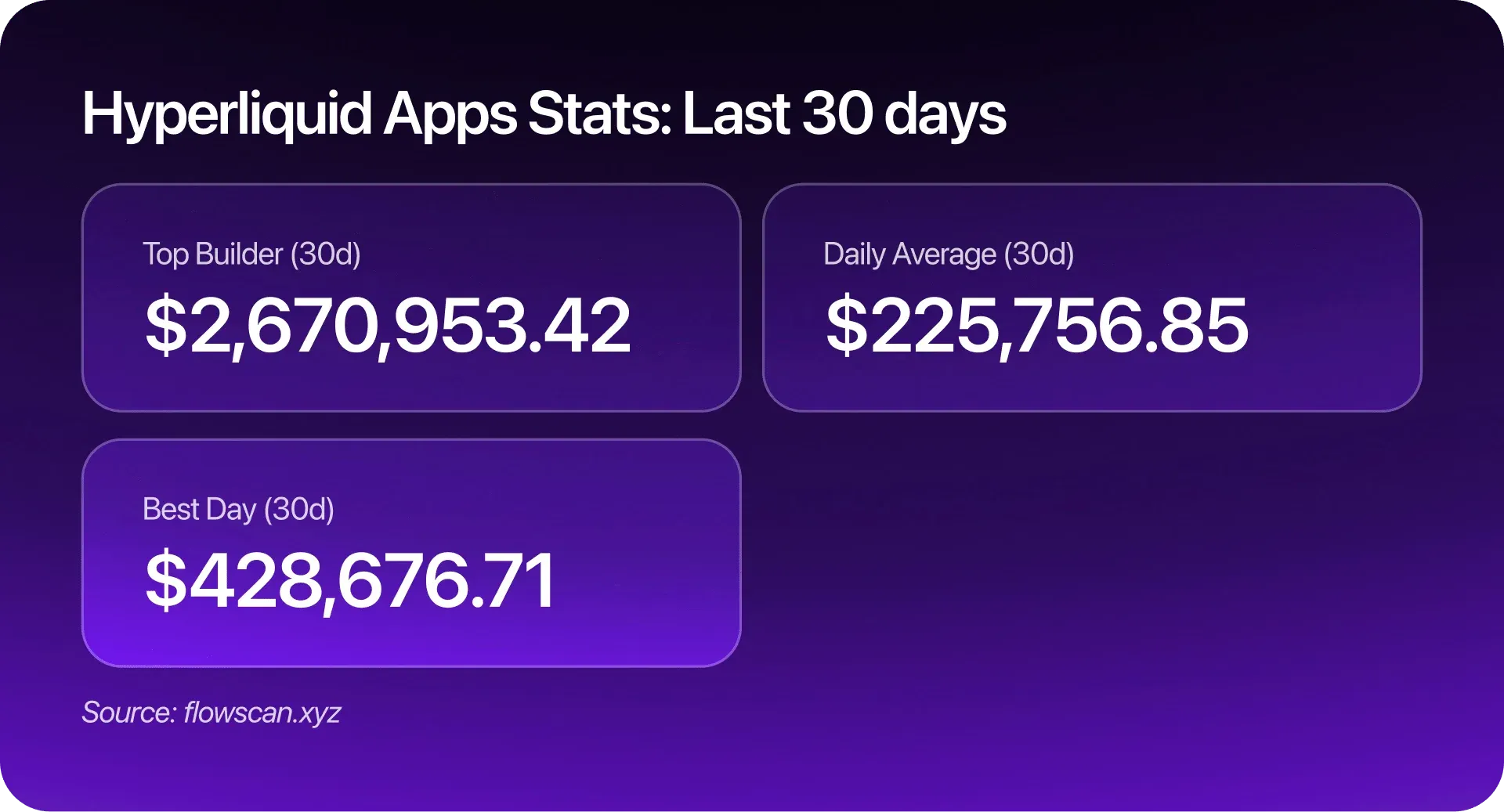

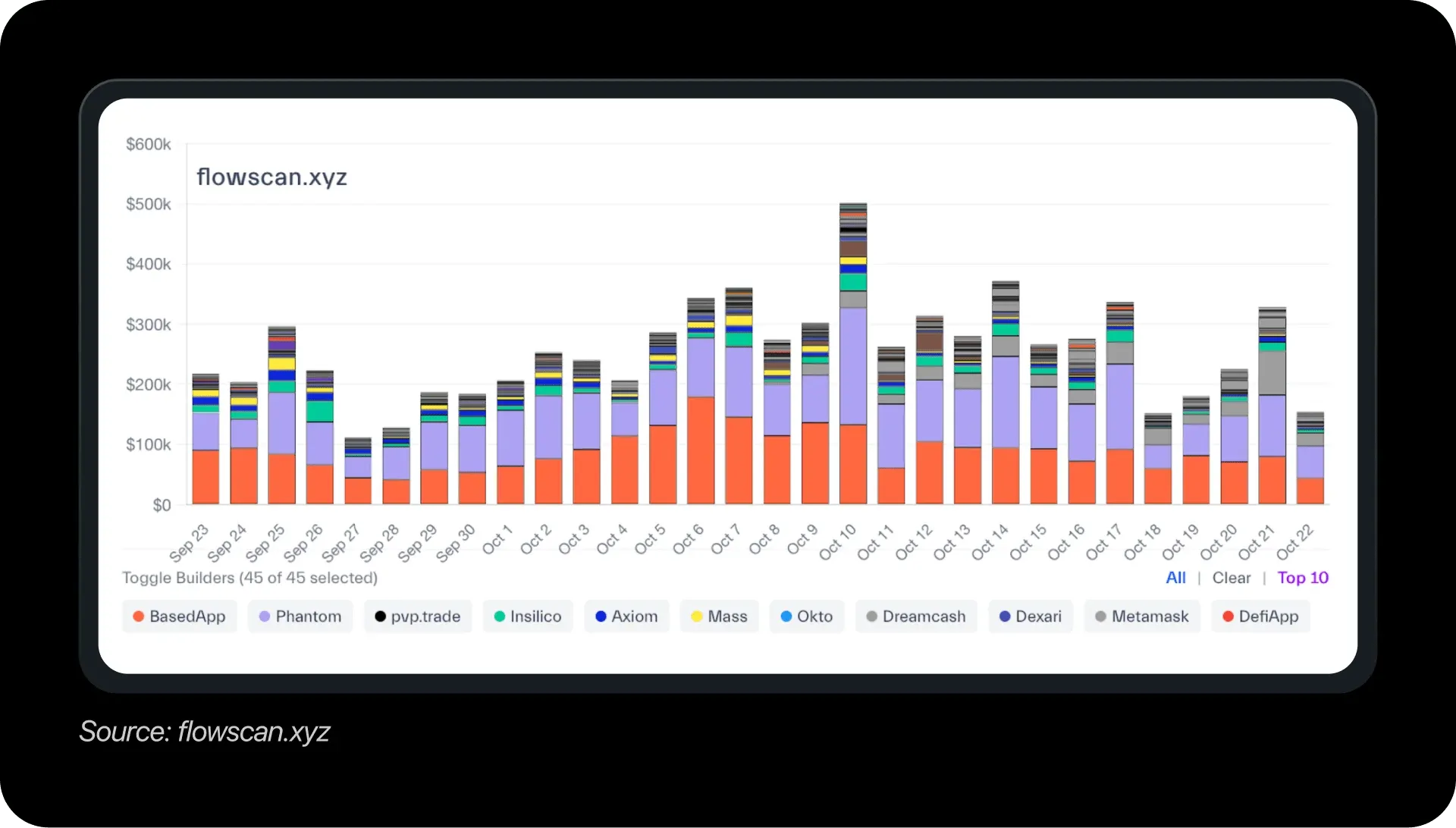

Over the past 30 days, Hyperliquid generated $7.7 million in new builder fees – an average of $256K per day, peaking at $502K. The payout curve has flattened from speculative bursts into a steady, repeatable cadence which is an indicator that the market is maturing and builder activity is no longer purely opportunistic.

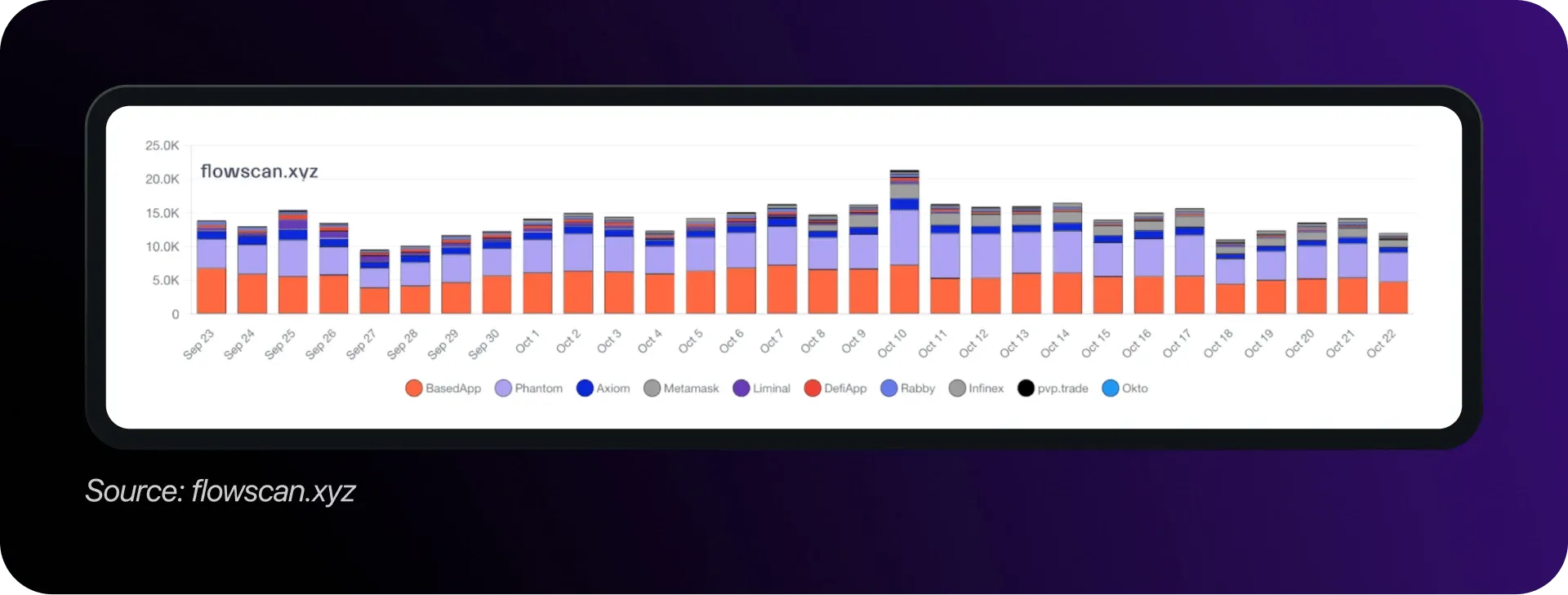

Average daily builder revenue now sits near $97K, while the network’s best day on record reached just over $1 million, a figure more typical of mid-tier centralized exchanges. The top builder alone (BasedApp) accounts for $9.1 million, or roughly 26% of all payouts.

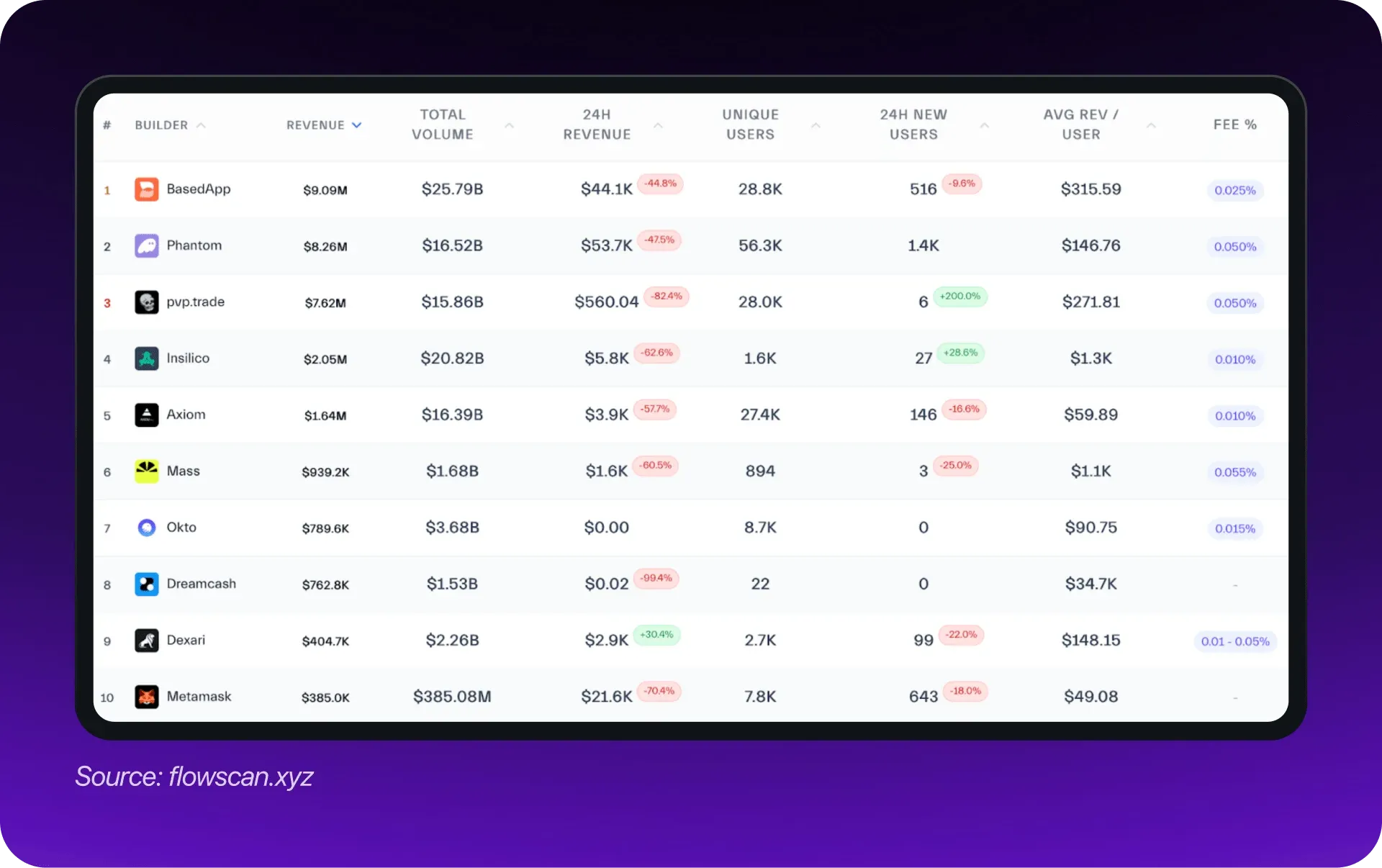

Top 10 Apps On Hyperliquid Today

Builder Dynamics — The Rise of Professional Front-Ends

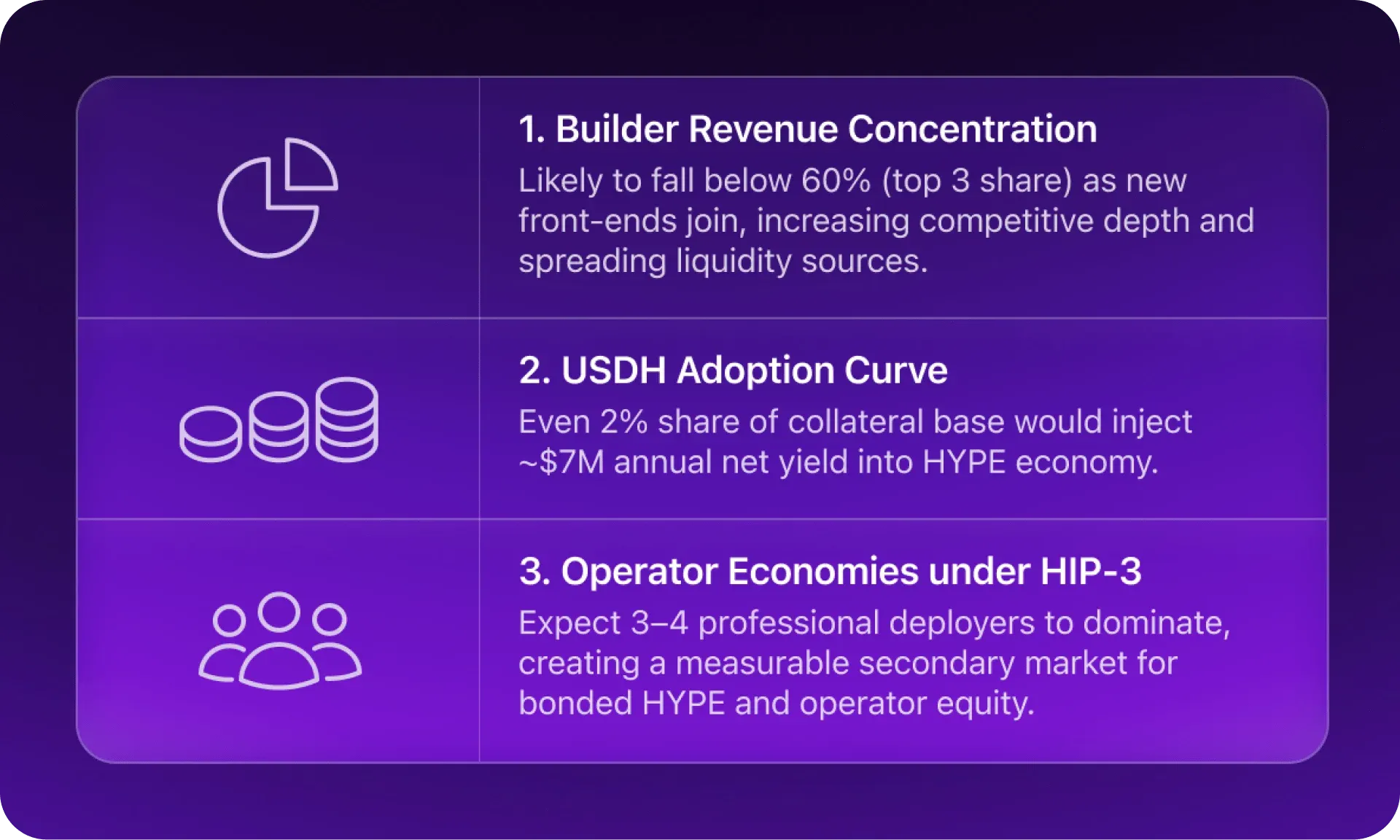

There are about 50 independent teams active on the network generating meaningful revenue, but ten control nearly the entire revenue pool. The top three — BasedApp, Phantom, and pvp.trade — collectively earned over $24 million, capturing roughly 70% of total builder fees.

Their growth trajectories reveal two different business models converging:

- Retail distribution plays such as Phantom and BasedApp thrive on user reach. Phantom alone has 56K unique users, generating a modest $147 ARPU, while BasedApp, with just 29K users, monetizes far more efficiently at $315 ARPU.

- Professional execution platforms like pvp.trade and Insilico attract far fewer users but earn orders of magnitude more per account. Insilico’s average user produced $1.3K in revenue, rivaling traditional brokerage economics.

Together, these patterns illustrate a bifurcated market: mass-market wallets drive liquidity inflow, while specialized trading terminals capture margin.

The two are symbiotic, volume discovery begins in wallets, but profits consolidate in execution-optimized UIs.

User Growth and Retention

The ecosystem has now onboarded 231K total users since inception, with many power users operating across multiple builders. User expansion has accelerated meaningfully since mid-September, coinciding with new builder launches and increased airdrop speculation.

More importantly, retention curves are improving. Phantom’s user cohorts show ~60% week-one and 26% week-four retention – on par with fintech benchmarks.

The shift from episodic to habitual trading behavior reflects that the platform has reached product–market fit with on-chain traders rather than just DeFi enthusiasts

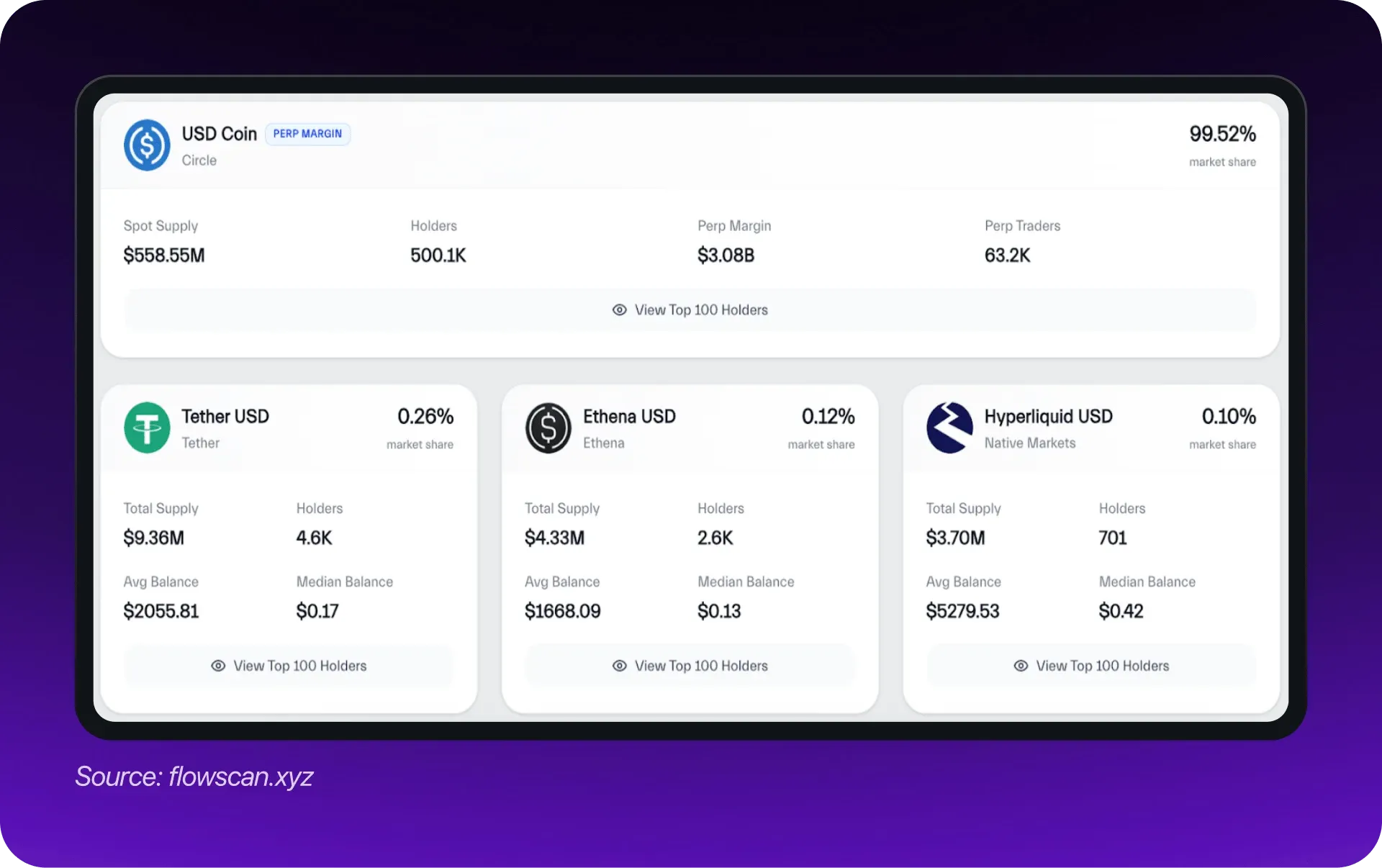

Stablecoin Composition — The Next Battleground

The Hyperliquid economy now holds $3.65 billion in stablecoin supply across ~508K wallets.

Stablecoin diversification is the next structural unlock. Capturing just 3% of margin collateral with a native yield-bearing unit could redirect eight figures of value back into the protocol economy.

The mix is highly concentrated: USDC accounts for 99.5% of collateral, with USDT, Ethena’s USDE, and Native Markets’ USDH dividing the remaining 0.5%.

While such dominance signals trust in Circle’s infrastructure, it also represents a missed economic opportunity – the yield on that float accrues off-chain. At prevailing Treasury rates, the externalized income equates to ≈ $180–200 million per year that could otherwise feed validator rewards or buybacks.

With USDH as default collateral and settlement, Hyperliquid reduces reliance on bridged stables. Native Markets plans a hybrid reserve model using short-term Treasuries (via BlackRock/Superstate) with audited transparency. Instead of yield leaking to USDC issuers, USDH channels it back into Hyperliquid – partly to the treasury, partly to HYPE buybacks.

Even a 2% share of the collateral base would inject ~$7M annual net yield into the HYPE economy.

USDH, though tiny at $3.7 million, is notable for its wallet profile: an average balance 5× larger than other stables, implying usage by professional operators rather than retail.

The Validator Layer and The HIP-3 Transition

Markets as Franchises: Hyperliquid’s validator layer now resembles an exchange operations team more than a typical proof-of-stake set. Their role is uptime, throughput, and sequencing integrity — the invisible infrastructure that keeps the on-chain exchange clockwork precise.

Validator activity remains steady with 24 active nodes securing 417.8 million HYPE at an average 2.17% APR.

The low inflation rate demonstrates that network security is now driven by real trading economics rather than issuance subsidies. Operational reliability has improved. Average block finality remains under one second, and even during peak liquidation events, validator miss rates stay below 0.2%. Three jailed validators over the past quarter indicate tightening slashing enforcement rather than systemic instability.

HIP-3 effectively turns HYPE staking into exchange franchising. Validators provide technical uptime; operators supply financial risk management; builders handle user acquisition. Hyperliquid’s architecture is evolving from a single DEX into a layered exchange economy

The upcoming HIP-3 upgrade will let any staker bond roughly 1 million HYPE to deploy a new perpetual market. While permissionless in theory, in practice only a handful of operators will meet the liquidity, risk, and uptime requirements.

Modeling current economics, a high-performing market operator processing $75 billion/month could earn roughly $450 million annualized gross fees, of which 10–15% flows to builders through routing codes.

If HIP-3 plays out as expected, a small group of competent deployers will run deep, liquid markets on top of Hyperliquid infra, while wallets and apps monetize through Builder Codes.

Comparative Market Structure and Outlook for Q4 2025

Among on-chain derivatives venues, Hyperliquid leads in nearly every measurable category:

- Hyperliquid’s matching engine now processes over $317 billion in 30-day notional volume, supported by $6.9 billion in open interest – the deepest of any on-chain derivatives venue – 2× Aster, 4× EdgeX.

- Daily perpetual volume averages $11–12 billion, up 30% month-over-month, ahead of Lighter ($10.4 B) and Aster ($10.9 B).

- Execution quality has become the platform’s defining moat.

- Rebalancing latency after large liquidations is sub-second (<400 ms), roughly matching Binance’s internal engine timing.

Aster excels in cross-chain presence (nine chains), and Lighter’s custom orderbook chain offers competitive speed, but both suffer from liquidity fragmentation. AMM venues such as Drift, Jupiter, and Ostium cater to retail but cannot sustain institutional position sizes.

Hyperliquid is doing to on-chain derivatives what Uniswap did to spot AMMs – standardizing liquidity into a single, composable state layer. Its advantage is structural: every marginal builder or operator deepens the same order book, compounding network effects.

Three quantitative signals define where momentum is heading:

Combined, these trends shift Hyperliquid from a single exchange protocol to an economic platform layer where developers, traders, and operators all monetize the same throughput flywheel.

Abhay M serves as SVP of Strategy and Investments at MoonPay, where he leads MoonVentures. MoonVentures encompasses MoonPay’s corporate investment arm as well as MoonPay Labs, the company’s accelerator program dedicated to nurturing entrepreneurial talent and innovation across the crypto ecosystem.