A new type of mortgage is emerging that allows crypto holders to use their digital assets as collateral when buying a home.

In March 2026, a crypto-backed mortgage structure supported by Fannie Mae was introduced, marking a new step in how crypto can be used in traditional finance.

What is Fannie Mae?

Fannie Mae is a government-sponsored enterprise overseen by the Federal Housing Finance Agency (FHFA). It buys loans from lenders and packages them into mortgage-backed securities.

Because Fannie Mae sets the standards that most lenders follow, its guidelines help determine which types of loans can be offered broadly across the U.S. housing market.

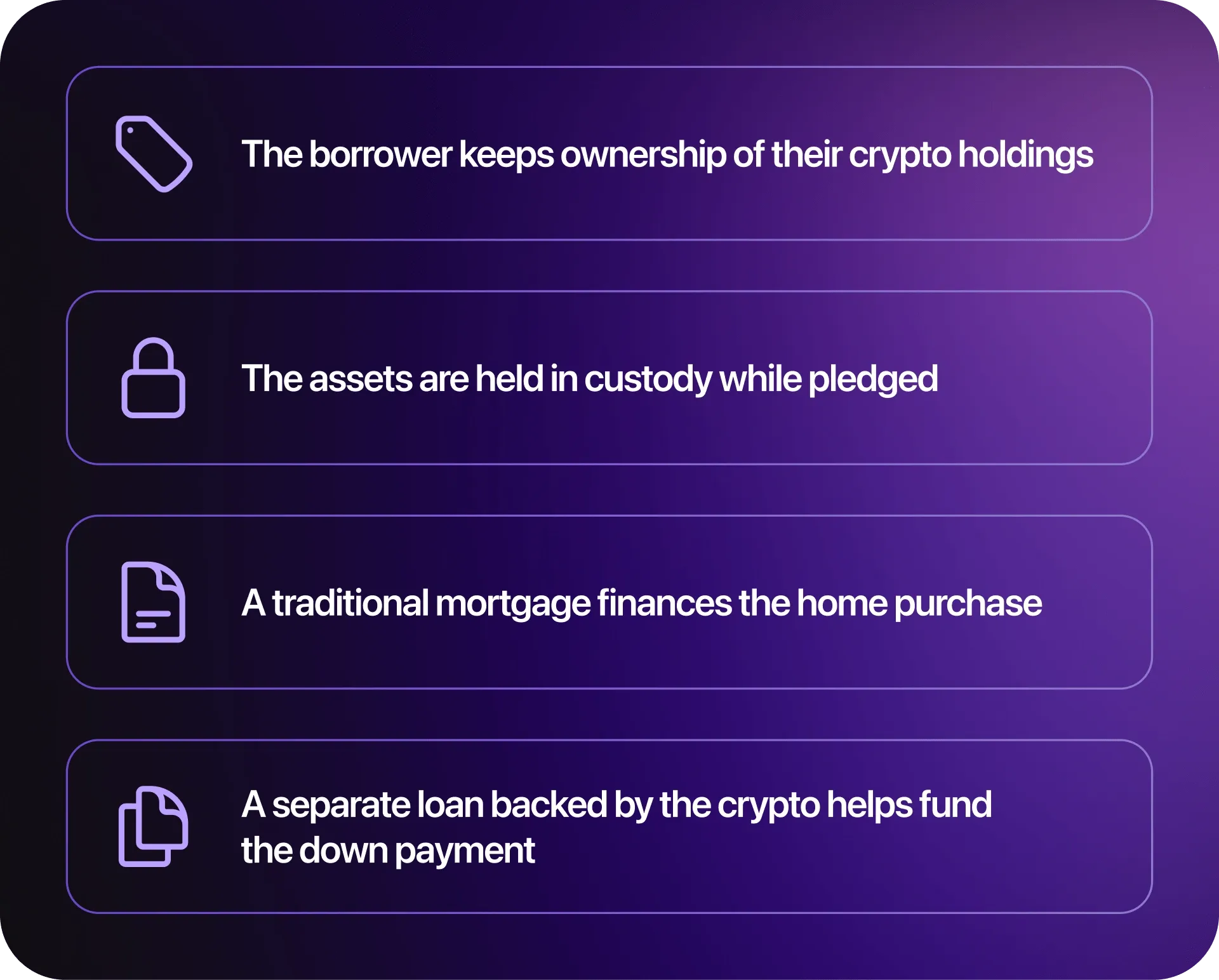

How crypto-backed mortgages work

Instead of selling crypto to fund a down payment, borrowers can pledge eligible digital assets as collateral.

In this structure:

Because the assets are pledged rather than sold, borrowers may be able to avoid triggering a taxable event, depending on their individual circumstances.

Why this matters

Traditionally, using crypto to buy a home required selling assets, which could trigger taxes and reduce long-term exposure.

Crypto-backed mortgages introduce an alternative approach, allowing borrowers to access liquidity without fully exiting their positions.

Earlier versions of these products were typically limited to a narrower group of borrowers. The involvement of a Fannie Mae-supported structure suggests this type of financing could expand over time.

What this means for crypto

Crypto-backed mortgages remain an early-stage product and are currently limited to specific platforms and eligibility requirements.

However, their introduction into the conforming mortgage system reflects a broader trend of digital assets being integrated into traditional financial services.

As new products are tested and refined, crypto is increasingly being used not just for trading or payments, but as collateral within established financial frameworks. Over time, similar structures may continue to develop alongside clearer regulatory and lending standards.