In a first-of-its-kind move, the U.S. Federal Housing Finance Agency (FHFA) has issued a directive to consider cryptocurrency as an asset when assessing risk for single-family mortgage loans delivered to Fannie Mae and Freddie Mac.

Yes—it’s real. Crypto for mortgages is no longer theoretical. It’s happening.

Wait—what is Fannie Mae and Freddie Mac?

Fannie Mae and Freddie Mac, officially the Federal National Mortgage Association (FNMA) and the Federal Home Loan Mortgage Corporation (FMCC) respectively, are government-sponsored enterprises (GSEs) that play a crucial role in the U.S. mortgage market. They purchase mortgages from lenders, package them into mortgage-backed securities, and sell them to investors—providing liquidity and stability across the system.

Essentially, they help keep the U.S. housing market liquid, stable, and affordable. Together, they support the majority of mortgages in the country.

Why now?

This move reflects growing demand to modernize mortgage lending in line with today’s digital-first financial lives, where crypto holdings are often a significant part of personal wealth.

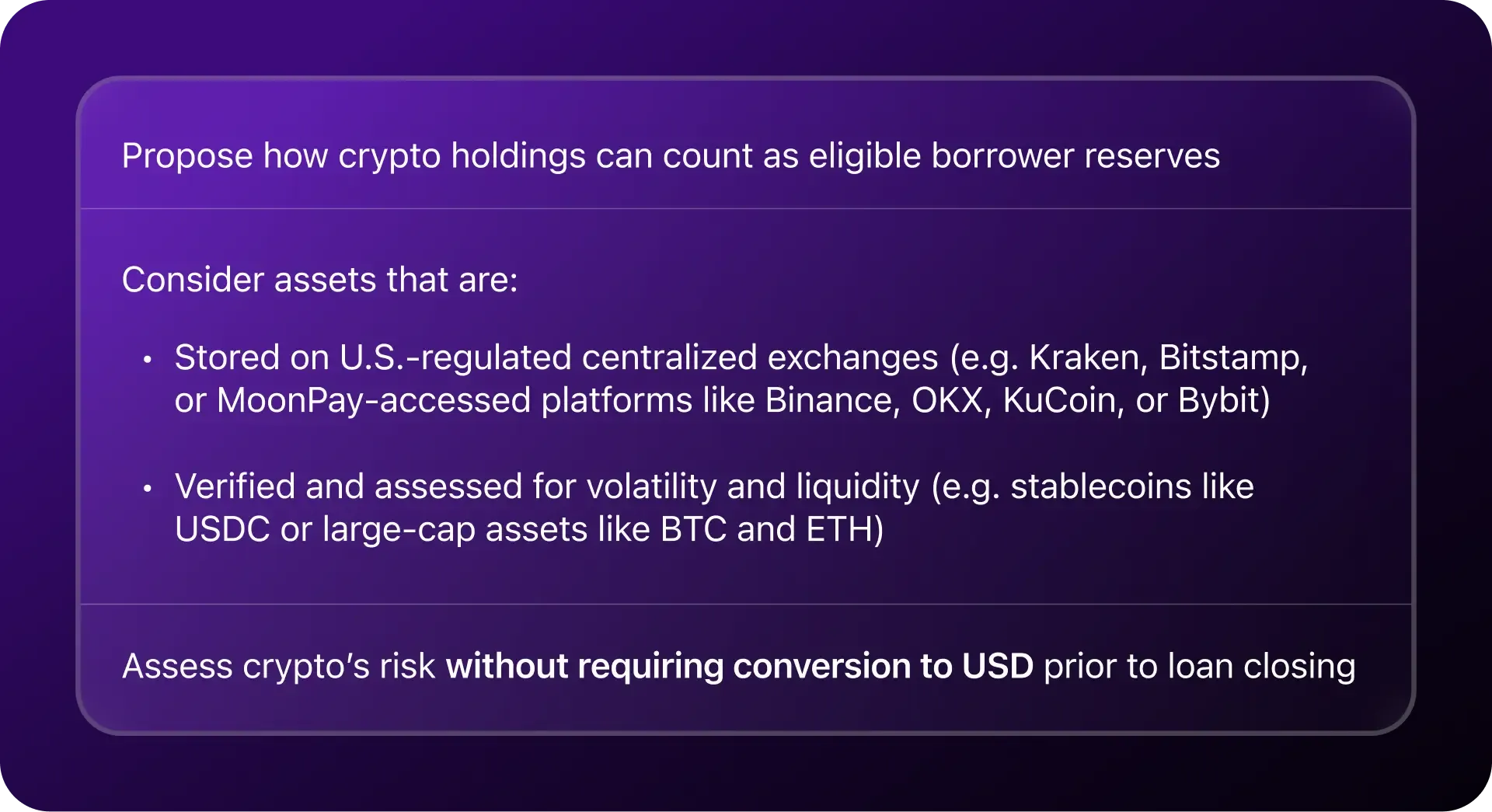

The Directive

Signed by FHFA Director William J. Pulte on June 25, 2025, the directive calls on Fannie Mae and Freddie Mac to:

“After significant studying, and in keeping with President Trump’s vision to make the United States the crypto capital of the world, today I ordered the Great Fannie Mae and Freddie Mac to prepare their businesses to count cryptocurrency as an asset for a mortgage.”

— William J. Pulte, FHFA Director

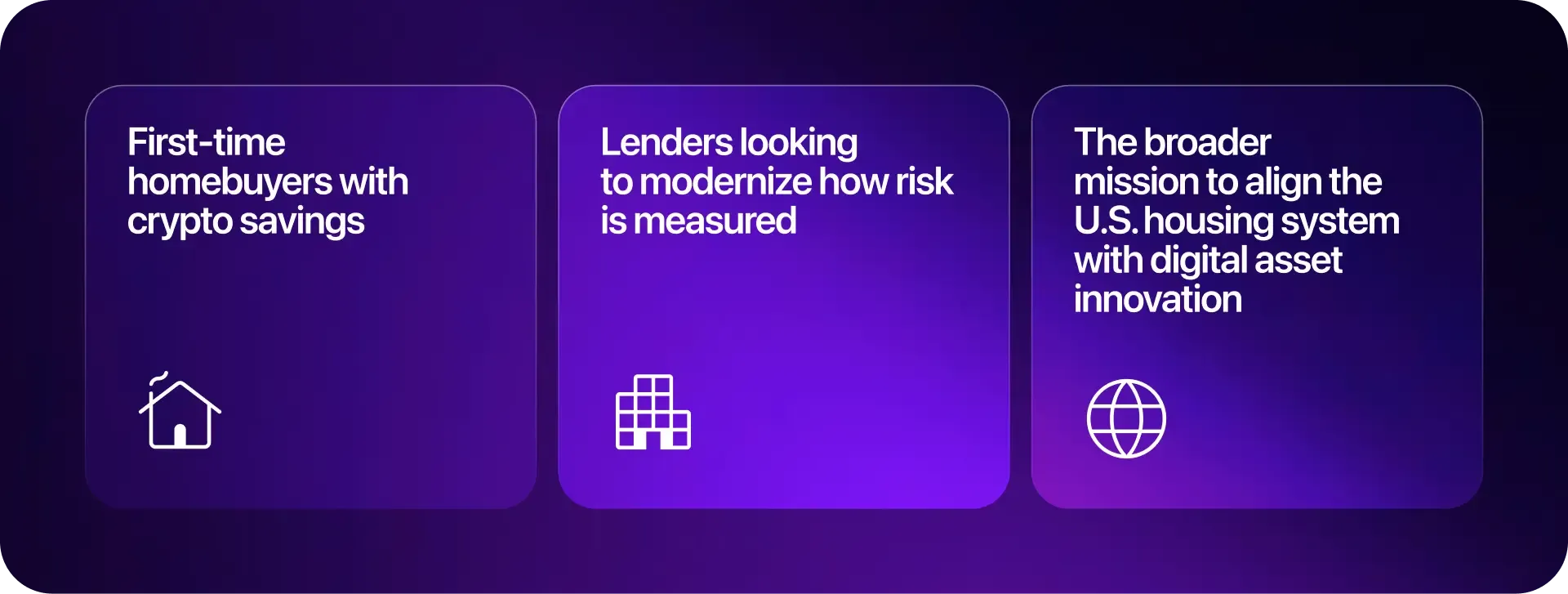

Why it matters

This directive could be a game changer for:

Until now, crypto holdings were excluded from reserve calculations—forcing borrowers to cash out and convert to USD just to qualify for a mortgage.

This order marks a potential turning point toward a more flexible, blockchain-inclusive housing finance system.

MoonPay’s Take

As crypto becomes more embedded in real-world finance—from retail payments to real estate—access matters more than ever.

That’s why we’re building infrastructure that lets people safely buy, hold, and use digital assets across wallets, chains, and now maybe... mortgages.

Crypto is evolving. Institutions are catching up.

At MoonPay, we’re ready to build the bridge—secure, scalable, and future-ready.